5 tectonic shifts in 2026

How they will impact us and our portfolio

Every year, I look for the big waves.

Not the short term noise.

Not the attention grabbing headlines.

The big structural changes.

Because when tectonic plates shift, the economy and markets move with them.

Using surfing as an analogy, there are always 2 sides to a big wave:

A complete wipe out, or, when one catches the right wave, you take off.

Applying this to investing and managing a portfolio:

Fortunes are made on one side of the wave, and lost on the other.

Historically, it’s normal to experience 1 big wave once every few years.

This year, I’ve identified 5 major waves or “tectonic shifts” that are currently underway.

1. The K-shaped economy is becoming the new economy

The K-shaped economy is no longer a phenomenon. It is becoming the economic system of both the United States and Canada.

In the US today, 50 percent of consumer spending is driven by just 10 percent of the population.

Half the spending.

From one tenth of the people.

Meanwhile in Canada, albeit at a less degree, the trend is trending toward the US, with the pandemic accelerating the recent trend.

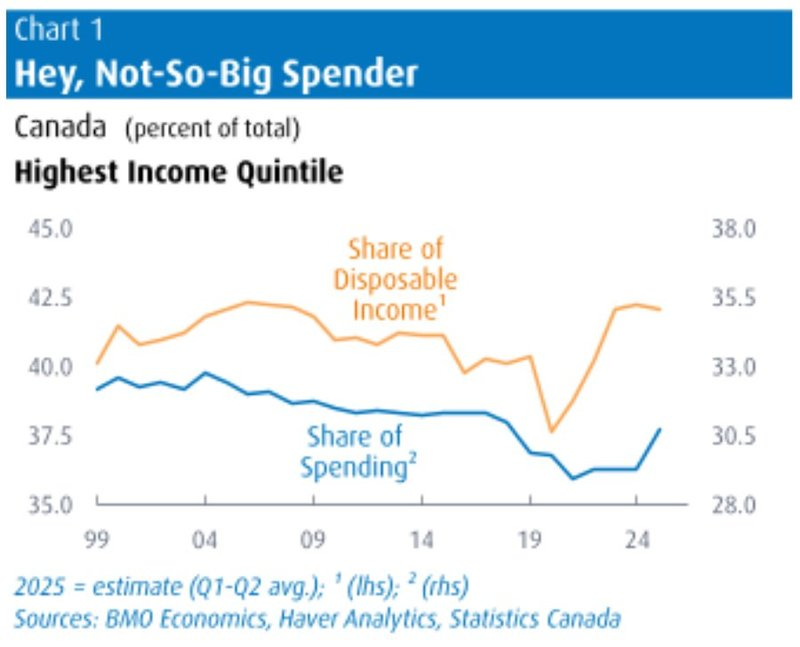

Statistics Canada finds that the top 20% of Canadian income earners account for 31% of total household spending, while the share of Disposable Income jumped significantly higher during the pandemic.

Asset owners have benefited from rising real estate prices, equity markets, owning businesses and even gold. Meanwhile, many middle class households are stretched by housing costs, debt, and stagnant purchasing power.

The US is simply further ahead on this curve.

Canada is playing catch up.

In both countries, asset inflation has rewarded those who own financial and real assets. Those without assets are relying solely on wages, and wages are not increasing at the same pace.

For our portfolio, the implications are clear:

Asset ownership remains critical

Exposure to quality equities and real assets continues to matter

The middle class squeeze is structural, not cyclical

The K-shaped economy is not a temporary phenomenon, it is becoming the new normal.

Over the coming years, the middle class is quickly disappearing.

Coming from a middle class family, this is sobering for me to write.

2. Stablecoins - The best gift from the blockchain technology

There has been rampant speculation and reckless gambling in the crypto space for many years.

Every time someone mentioned meme coins as assets, I cringe.

While I believe most meme coins have little value, a real, legitimate use case of crypto technology has been quietly taking over the world.

Most people still think of Visa, MasterCard, and Amex when they think of payments.

But as of 2024, Stablecoins have outpaced Visa as the number one transaction payment processor in the world!

Processing roughly 16 trillion dollars in volume.

This is not a small shift.

This is a tectonic shift.

A Stablecoin is a cryptocurrency tied to a stable asset such as the US dollar or gold, using blockchain technology but without the volatility of Bitcoin.

Adoption is accelerating globally, especially outside North America. As usage grows:

More capital flows into assets backing Stablecoins, such as US Treasuries or gold

Traditional remittance and payment businesses are facing real competitions

Bitcoin’s dominance may weaken as Stablecoins being used for every day transactions

If you own payment companies, understand the disruption risk.

If you own Bitcoin, understand the competitive landscape is evolving.

The part that may be surprising many North American investors:

The wave is already here.

3. The GLP-1 economy

Most people think GLP-1 is just a weight loss drug.

It is much bigger than that.

US obesity rates have climbed from roughly 30 percent in the early 2000s to 42 percent around 2020. Even childhood obesity has surged toward 20 percent.

Now, one in eight US adults is taking a GLP-1 drug.

The drug is reaching mass adoption rapidly.

What’s most interesting about GLP-1 drugs is the impact on the rewards circuitry in our brain.

That means, many of the addictive behaviors will now be better regulated while on the medication.

This is similar to when smartphones reshaped communication. The direct impact is straight forward: convenience, accessibility.

However, the second and third order effects are where they’re not as obvious, such as:

The boom of ride share companies such as Uber, or impact to interpersonal relationship.

Here’s what we will be watching:

Restaurants

Airline profits

Gym / wellness

Plastic surgery

Companies exposed to declining consumption patterns

Productivity and labor participation

This is not a diet fad. It is a structural health and economic shift reversing years of health trend.

4. White collar recession, blue collar boom in the AI economy

AI is reshaping the labor market in real time.

White collar job openings in areas such as software development, business analysis, and data roles have all dropped significantly, in many cases by nearly two times.

At the same time:

Healthcare added 82,000 jobs

Social assistance added 42,000

Construction added 33,000

Blue collar is winning in the current AI economy.

White collar wages have plateaued and are starting to decline. Long term wage deflation in certain knowledge based roles is a real possibility.

For the first time in history, knowledge is becoming cheaper, not more valuable, because AI can replicate many tasks that used to require a university degree.

That is a profound shift.

Implications for investors:

Real estate in traditionally white collar neighborhoods may face pressure.

Blue collar regions tied to construction, infrastructure, and healthcare will be seeing tailwinds.

The modern society as we know it will be changed forever.

5. The rise of teenage millionaires and soon billionaires

We are entering an era where teenagers are building seven to eight figure net worths.

We are already seeing teenager such as Ryan Kaji with an estimated net worth between 100 to 130 million dollars through platforms like YouTube.

Top creators on platforms such as Roblox are earning on average 23 million dollars per year, many of them from Gen Alpha and Gen Z .

We have also seen the emergence of extremely young self made billionaires in their 20s.

Digital platforms have removed gatekeepers.

Distribution is global.

Capital formation is faster than ever.

This is another major structural change to our society that will be new to all of us.

For families, this changes parenting.

For investors, this changes where value is created.

The next generation will not build wealth the same way previous generations did.

They will build it online with AI.

At speed.

At scale.

I believe the future will be an exciting place for those who are prepared

It may feel overwhelming in the moment while we’re transitioning into a new reality.

Throughout history, we have seen a future that is better than the past.

In a few years, extreme poverty is projected to be eliminated from our awareness.

Life expectancy is expected to increase as health care continue to innovate with AI.

My intention of sharing these “tectonic shifts” with you is simple:

To help you be aware of what’s appearing on the horizon and capitalize the opportunities that await us.

You can still catch the replay of my 2026 Economy and Market Predictions until the end of February:

https://2026predictions.fromericchang.com/

If you like my work, I invite you to share it with others.

Eric Chang

Cardston, Alberta, Canada

February 24, 2026

Copyright © 2026 EC Research Group.

No part of this publication may be reproduced, distributed, or transmitted in any form or by any means, including photocopying, recording, or other electronic or mechanical methods, without the prior written permission of the publisher, except in the case of brief quotations embodied in critical reviews and certain other noncommercial uses permitted by copyright law.

The information provided herein is believed to be accurate and reliable, but EC Research Group does not guarantee its accuracy or completeness. The content is for informational purposes only and is not intended to be a substitute for professional financial advice. EC Research Group is not a financial advisor and does not provide personalized financial advice. The views and opinions expressed in this publication are those of the author and do not necessarily reflect the official policy or position of EC Research Group. The content may be subject to change without notice and may become outdated over time. EC Research Group is under no obligation to update or revise any information presented herein.

Investments involve risks, and individuals should consult with a qualified financial advisor before making any investment decisions. Prospective investors should carefully consider the investment objectives, risks, charges, and expenses of any investment before investing.