Bonds quit working

My chat with an ex 140M+ Financial Advisor

A bit of delay in publishing today’s newsletter.

I had a packed schedule of meetings today.

One of the meetings, was with a Financial Advisor of 21 years.

He started in this business when he was 26 years old!

Before selling his practice last year, he was managing over $140 million USD in AUM.

For those unfamiliar with the term, AUM stands for Assets Under Management.

We connected over our shared views.

Both of us are seeing the same thing:

Investors today are taking on enormous risks.

Many of them without realizing it.

Who can blame them?

For the past 17 years, the market has mostly gone in one direction:

Up. Up. Up.

Many younger Millennials, and older Gen Zs have never seen a market crash before.

How would anyone believe in Unicorn if they have never seen one before?

During our chat, the Advisor said something I’ve heard from many professional Money Managers lately:

“I’ve seen this movie before.”

Many investors were raised on the 60/40 portfolio

For decades, investors were taught a simple model:

The 60/40 portfolio.

60% stocks.

40% Bonds.

Simple. Reliable. Effective.

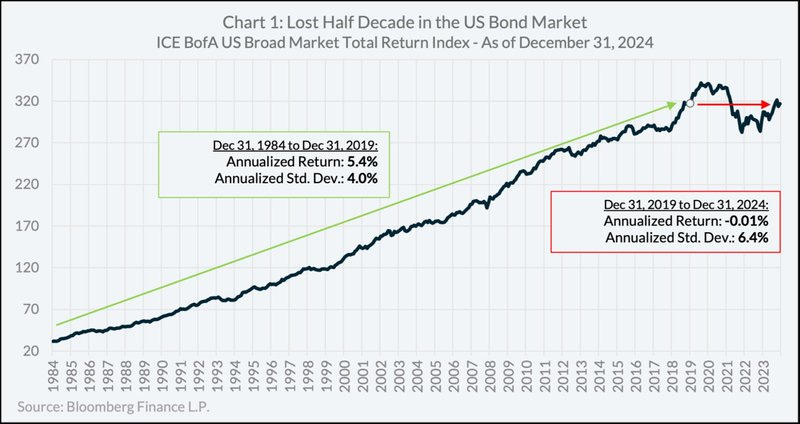

For around 40 years, it worked beautifully.

But there was an important reason why:

The rule never changed.

From the early 1980s until 2020, the global economy experienced one of the biggest trends in financial history:

Falling interest rates.

A quick refresher:

Bond prices and interest rates have an inverse relationship.

When interest rates go down, Bond prices go up.

When interest rates go up, Bond prices go down.

In the early 1980s, interest rates were at historic highs.

Since then, they have mostly moved downward for four decades.

That meant Bond prices were rising for nearly 40 years.

Image Credit: Lysander Funds

No wonder Bonds worked so well.

They weren’t just defensive. They were also profitable.

Then COVID happened and everything changed.

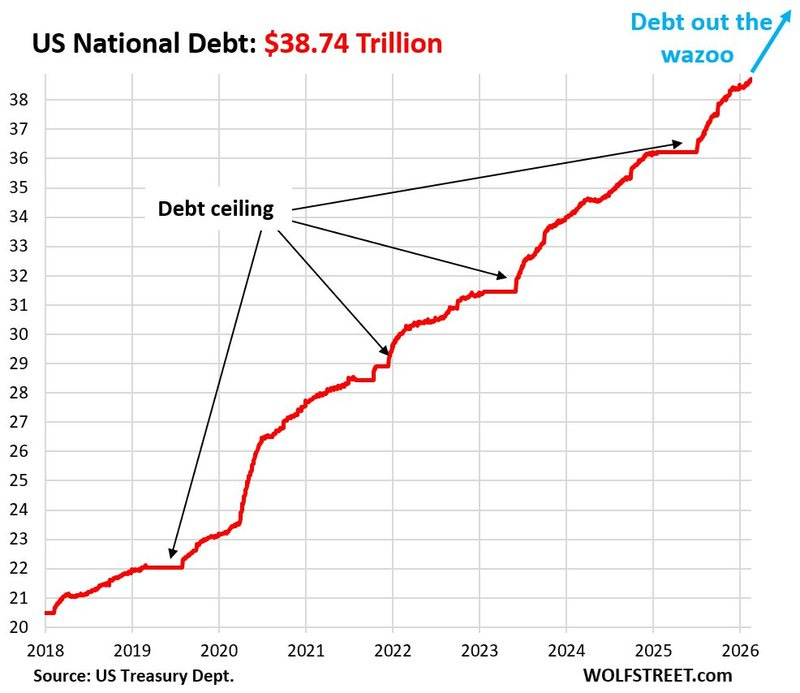

Governments around the world did something unprecedented during COVID.

They took on more debt in a few short years than they had accumulated over decades, even centuries.

Take the United States as an example.

The national debt exploded during the pandemic.

In fact, the increase almost doubled during COVID than the entire 250 years since the country’s independence.

Image Credit: Wolf Street

Governments worldwide accomplished this by printing money.

An insane amount.

But money printing never disappears quietly.

All that cash eventually shows up somewhere.

Most often, it appears in its ugliest form:

Inflation.

COVID flipped the old playbook on its head.

The rules have changed.

And whenever the structure of the economy changes, we have to throw out the previous playbook.

That’s uncomfortable.

Especially when it comes to our wealth.

“We’ll be fine”

There’s a story from the book “Losing the Signal: The Untold Story Behind the Extraordinary Rise and Spectacular Fall of BlackBerry.”

After Apple introduced the iPhone to the world, the next day, BlackBerry (Research In Motion) co-CEO Mike Lazaridis pulled his partner Jim Balsillie in front of a computer.

“Jim, I want you to watch this,” he said, pointing to a webcast of the iPhone unveiling.

[…]

“These guys are really, really good,” Mr. Lazaridis replied. “This is different.”

“It’s OK—we’ll be fine,” Mr. Balsillie responded.

“We’ll be fine.”

Those words would later haunt the company.

Within a few short years, BlackBerry went from market dominance to irrelevance.

Why?

Because they assumed the old rules still applied.

They didn’t.

The world had changed.

And they didn’t adapt fast enough.

The conversation with the former $140M advisor reminded me of that story.

He believes Bonds are no longer serving investors the way they had in the past.

Within the next few years, the classic 60/40 portfolio could slowly fade away.

“We’ll be fine.”

It’s a movie we’ve seen before.

Massive Government Deficits

During this interview, Louis Gave of Gavekal Research pointed out why he also believes The 60/40 Portfolio Is Dead.

The world’s largest economies are running massive budget deficits while economies aren’t in a severe recessions or major conflicts.

China, for example, is running a deficit around 10% of GDP.

The United States is running deficits around 6% of GDP.

European economies are largely between 2% and 4.5%.

Japan continues to expand fiscal spending aggressively.

Across the world, governments are stepping on the same gas paddle:

More and more fiscal stimulus.

When governments spend at these levels while central banks maintain loose monetary policy, it creates higher inflation.

And inflation quietly erodes the real value of fixed-income assets.

In other words:

Bonds.

In an environment like this, Bonds may no longer function the way investors expect them to.

The policy environment has shifted toward something far more inflationary.

And that changes the rules of the game.

Bonds are no longer protecting against stock declines

The beauty of the 60/40 portfolio was its simplicity.

When stocks fell during economic uncertainty, Bonds usually rose.

Investors usually sell higher risk assets such as stocks and move capital into less volatile assets such as Bonds.

The two assets moved in opposite directions.

That meant investors could rebalance periodically and enjoy stable returns.

Gave called it:

“Rebalance every quarter and go to the beach.”

It worked for decades.

But that relationship breaks down during “energy shock” or an inflationary regime change.

A perfect example happened in 2022.

When Russia invaded Ukraine, energy prices surged.

Oil skyrocketed.

Inflation fears crept into the market.

And suddenly, something unusual happened:

Stocks fell.

Bonds fell too.

The diversification benefit disappeared.

Instead of protecting portfolios against stocks decline, Bonds joined the decline.

Investors had nowhere to hide under the 60/40 portfolio.

Over the past week, we’ve seen this script played out again with the war with Iran:

Stocks struggled.

But Bonds also dropped.

For investors relying on the classic 60/40 model, the protection wasn’t there.

Rules are changing

Markets evolve.

Economic climate change.

Investment strategies that worked for decades can suddenly stop working.

The investors who thrive are not the ones who cling to the past.

They are the ones who recognize when the wind changes direction and adjust their sails accordingly.

Or as we said this many times before:

Skate to where the puck is going, not where it has been.

Because when the rules change, the old playbook stops working.

And those who fail to adapt often learn the lesson the hard way.

If you like my work, I invite you to share it with others.

Eric Chang

Edmonton, Alberta, Canada

March 10, 2026

Copyright © 2026 EC Research Group.

No part of this publication may be reproduced, distributed, or transmitted in any form or by any means, including photocopying, recording, or other electronic or mechanical methods, without the prior written permission of the publisher, except in the case of brief quotations embodied in critical reviews and certain other noncommercial uses permitted by copyright law.

The information provided herein is believed to be accurate and reliable, but EC Research Group does not guarantee its accuracy or completeness. The content is for informational purposes only and is not intended to be a substitute for professional financial advice. EC Research Group is not a financial advisor and does not provide personalized financial advice. The views and opinions expressed in this publication are those of the author and do not necessarily reflect the official policy or position of EC Research Group. The content may be subject to change without notice and may become outdated over time. EC Research Group is under no obligation to update or revise any information presented herein.

Investments involve risks, and individuals should consult with a qualified financial advisor before making any investment decisions. Prospective investors should carefully consider the investment objectives, risks, charges, and expenses of any investment before investing.