Great article. Are you buying any?

Unpacking how I look at SpaceX IPO's risks vs. rewards

Thanks for your patience as I delayed publishing this week’s newsletter. I was away yesterday hosting an event launching our new fund.

Several readers wrote me messages after last week’s newsletter:

https://www.ecresearchgroup.com/p/elon-musks-ipo-game

“Great article. So are you buying any?” - Reader Nadine R.

“Great article on IPO you sent out. You left me hanging! So does that mean your planning on buying in on IPO on June 12th?” - Reader Ryan O.

I didn’t mean to leave anyone hanging.

The short answer: I didn’t buy the IPO.

As to why, we’ll unpack it in today’s newsletter.

We wrote about looking for Asymmetrical opportunities before

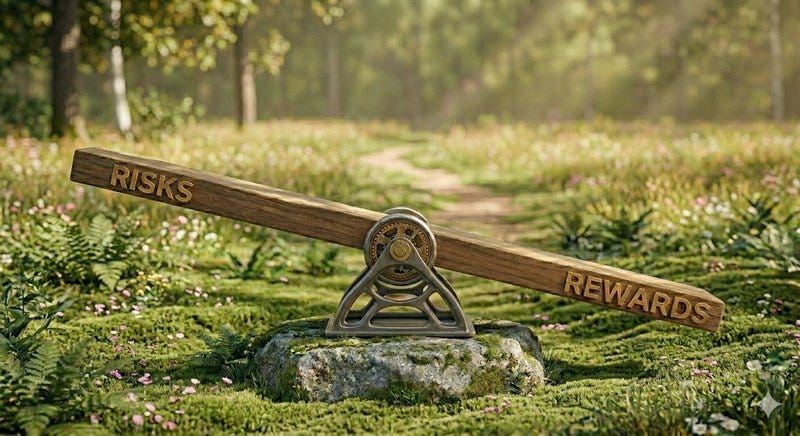

A quick refresher on what Asymmetrical means.

Using a seesaw as a visual, we’re looking for a tilted seesaw, where the potential reward outweighs the underlying risk.

What are asymmetrical returns?

These are the Holy Grail of investing. The unicorns.

An asymmetric trade or asymmetric payoff is when the outcome of a trade has more profit than loss or risk taken to achieve the profit. Or, the upside potential is greater than the downside loss.

Asymmetry of a trade may be when the downside is limited, but the upside is unlimited.

Or, if we are speaking of an asymmetric outcome, the upside profit was greater than the amount risked.

We also shared an example of asymmetrical reward vs. risk in real estate here:

https://www.ecresearchgroup.com/p/theres-a-reason-theyre-lowering-rates

So when a reader asks if I’m buying the IPO, the real question I’m asking myself is simpler: Is the seesaw tilted in my favor?

Let’s look at three concerns.

Concern #1: Sky high valuation

At roughly $1.77 trillion against 2025 consolidated revenue of about $18.7 billion, the stock trades at around 100x sales.

After the IPO pop, the valuation only got more stretched.

Today, SpaceX’s valuation is approximately $2.52 trillion, putting the stock at around 135x sales.

Think about what 135x sales actually means.

You’re paying 135 dollars for every single dollar of revenue that walks in the door, and that revenue isn’t even profit yet.

At that price, investors aren’t valuing a business. They’re valuing a story about the future, decades out, and assuming almost none of it goes wrong.

Concern #2: It’s not profitable. The AI unit is burning through cash

In 2025 SpaceX reported a loss from operations of about $2.6 billion despite roughly $6.6 billion in adjusted EBITDA, and Q1 2026 showed a $1.9 billion operating loss on $4.7 billion revenue.

Elon consolidated xAI/X into SpaceX. The AI unit spent $7.72 billion in Q1 2026 alone and posted a $2.47 billion operating loss in that quarter.

The AI unit invested/spent more in a single quarter than the entire company brought in as revenue for that same quarter.

This is the part that troubles me. When you fold a cash-incinerating AI business into the crown jewel, you don’t make the business stronger.

So now the rocket company has to keep feeding the AI furnace. And every dollar shoveled into that furnace is a dollar that isn’t being returned to the people buying in at 135x sales.

Profitable companies can survive a bad year. Companies burning billions a quarter survive only as long as someone keeps funding the burn. Those are two very different risk profiles.

Concern #3: Key-person risk

The biggest risk of all: SpaceX’s extreme rich valuation is entirely dependent on Elon Musk.

He is a genius. There’s no doubt about it.

Unfortunately, a genius is no different than any other human. They are mortal.

There’s no succession plan that replaces a founder the market treats as irreplaceable. That’s the whole problem. The premium investors are paying, in large part, is a bet on one man’s life.

When the thesis can’t survive without a single human being, that isn’t a moat. It’s a single point of failure.

Priced for perfection

I have nothing against SpaceX or Elon Musk.

What I am against is overpaying for an investment.

When an asset is priced extremely high, it doesn’t leave a lot of room for surprises.

Any business owner will tell you, there’s always surprises when it comes to running a company.

Sometimes there are mistakes the company makes.

Sometimes it has nothing to do with the company itself such as a black swan event. A highly unpredictable occurrence that lies far beyond the realm of normal expectations, carrying a massive impact.

When an asset is valued like SpaceX, it’s no longer driven by fundamentals. It’s driven by investor speculation.

This is the exact opposite of an asymmetrical opportunity.

More like asymmetrical risk to a unit of return earned.

It doesn’t mean an investor can’t make a return from the asset. As long as there’s another investor willing to pay an even higher price, it can continue to rocket higher (no pun intended).

This is called the greater fool theory.

In finance, the greater fool theory suggests that one can sometimes make money through speculation on overvalued assets (items with a purchase price drastically exceeding the intrinsic value) if those assets can later be resold at an even higher price.

The question I have for you: Who is the fool, and who’s going to be the greater fool?

If you like my work, I invite you to share it with others.

Eric Chang

Calgary, Alberta

June 17, 2026

Copyright © 2026 EC Research Group.

No part of this publication may be reproduced, distributed, or transmitted in any form or by any means, including photocopying, recording, or other electronic or mechanical methods, without the prior written permission of the publisher, except in the case of brief quotations embodied in critical reviews and certain other noncommercial uses permitted by copyright law.

The information provided herein is believed to be accurate and reliable, but EC Research Group does not guarantee its accuracy or completeness. The content is for informational purposes only and is not intended to be a substitute for professional financial advice. EC Research Group is not a financial advisor and does not provide personalized financial advice. The views and opinions expressed in this publication are those of the author and do not necessarily reflect the official policy or position of EC Research Group. The content may be subject to change without notice and may become outdated over time. EC Research Group is under no obligation to update or revise any information presented herein.

Investments involve risks, and individuals should consult with a qualified financial advisor before making any investment decisions. Prospective investors should carefully consider the investment objectives, risks, charges, and expenses of any investment before investing.