IPOs are for the insiders to get rich

The buzz fades

IPOs are exciting.

There is something magnetic about watching a private company step into the public spotlight.

Right now, three of the biggest names in technology are lining up to go public: SpaceX (parent company of Starlink), OpenAI (Chat GPT), and Anthropic (Claude AI). SpaceX alone is eyeing a valuation near $1.75 trillion. The financial press is buzzing. Everyday investors are getting excited.

But before you get swept up in the excitement, let me share what the history books actually say about buying into IPOs.

Because the story is not what most people think.

What is an IPO?

IPO stands for Initial Public Offering. It is the process by which a private company sells shares to the public for the first time.

For the founders, early employees, and venture capital investors who have been holding equity for years, an IPO is a liquidity event. It is their moment to convert paper wealth into real money.

For the public investor, it is a chance to buy in on a company they believe in.

That asymmetry matters. And we will come back to it.

The mechanics work like this: investment banks underwrite the offering, setting an offer price before the stock begins trading. Institutional investors, hedge funds, and insiders get access to shares at that offer price. By the time the stock opens on a public exchange, retail investors are buying in the secondary market at whatever price the stock has already moved to.

The insiders (early investors, founders, employees) get in at the ground floor. IPO insiders get in on the 70th floor. Everyone else try to catch the escalator up after that.

We saw record numbers of companies going public before the dot-com bubble burst

The late 1990s were a gold rush.

Every week, another internet company went public. Valuations had little to do with earnings or revenue. They were powered entirely by narrative and momentum. The word “dot-com” attached to any business was enough to send a stock soaring on its first day of trading.

Between 1995 and 2000, the US IPO market exploded. Hundreds of companies flooded the public markets. Many had no path to profitability. Some had no revenue at all. It didn’t matter. Investors were chasing the story.

Then the music stopped.

When the bubble burst, the laggards were holding the bag. The insiders had already cashed out. Retail investors were left with worthless paper.

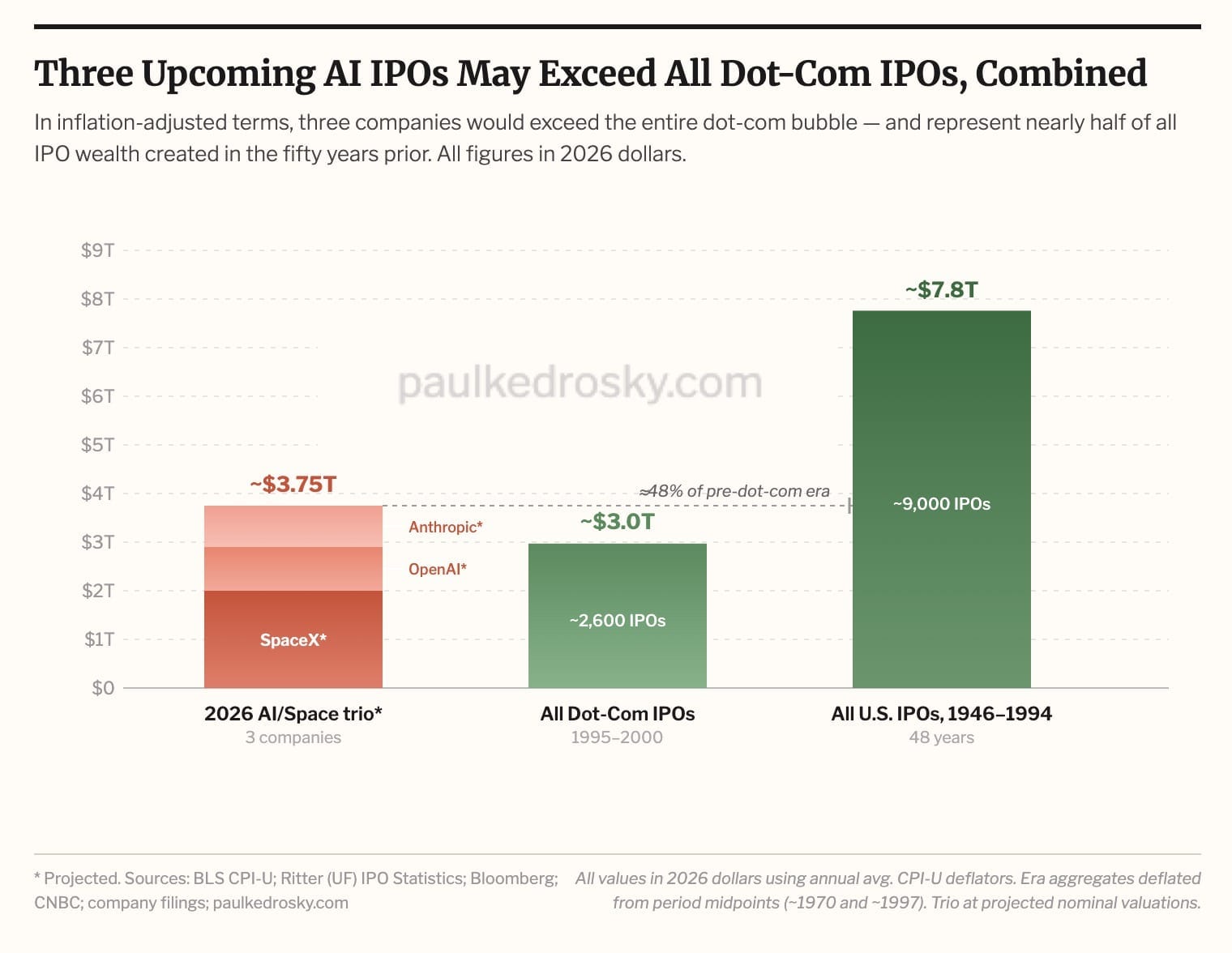

This time we’re seeing potentially record amounts of capital raised from IPOs

This time, these companies actually have real product, revenue and strong business models.

SpaceX, OpenAI, and Anthropic are all expected to go public in the coming months. In inflation-adjusted terms, SpaceX alone would rank as the second-largest IPO in history, just behind Saudi Aramco. All three together would exceed the entire dot-com IPO wave of 1995 to 2000.

But there is a problem that most people are not talking about.

That much new equity supply hitting in a few months creates a math problem: the money has to come from somewhere. Most of it will come from existing holdings. Passive funds will be forced buyers once these names join the indexes, which will happen much faster than usual, given recent index rule changes. That means mechanical selling pressure on whatever many funds currently own, which is mostly the same large-cap tech stocks everyone else owns.

Source: https://paulkedrosky.com/the-coming-mega-ipo-flow-funding-problem-of-2026/

In other words, the very act of these companies going public could trigger a rotation out of the stocks most investors already hold. The excitement of the new is funded by selling the old.

IPOs are for the insiders to get rich

Here is the uncomfortable truth Wall Street or Bay Street will not tell you.

The IPO process is designed, first and foremost, to reward the people who were already there. Founders. Early employees. Venture capital firms. Private equity. They have been waiting years for this moment. They got in from the ground floor. The IPO is their exit.

The offer price is set by investment bankers working for the company. Shares at that price go to institutional clients first. By the time you log into your brokerage account to buy, the price has already moved.

You are not getting in early. You are getting in after the insiders have already locked in their gains.

IPO stock prices can be extremely volatile and are often impacted by structural characteristics such as a small float, lock-up periods, and limited operating histories. The headline market capitalization is simply the share price multiplied by total shares outstanding, while the float-adjusted market capitalization reflects only the shares actually available to public investors after excluding founder, insider, and other strategic or control holdings. A company can debut at a $1 trillion-plus valuation yet float only 5 to 10 percent of its shares, resulting in a relatively small number of shares available for trading and potentially amplifying price swings.

Pre-IPO investors often have lock-up periods restricting them from selling for a set time. When those lock-ups expire, early investors may exit. That selling pressure lands on the public investors who bought in at the peak of the excitement.

You are the liquidity they needed.

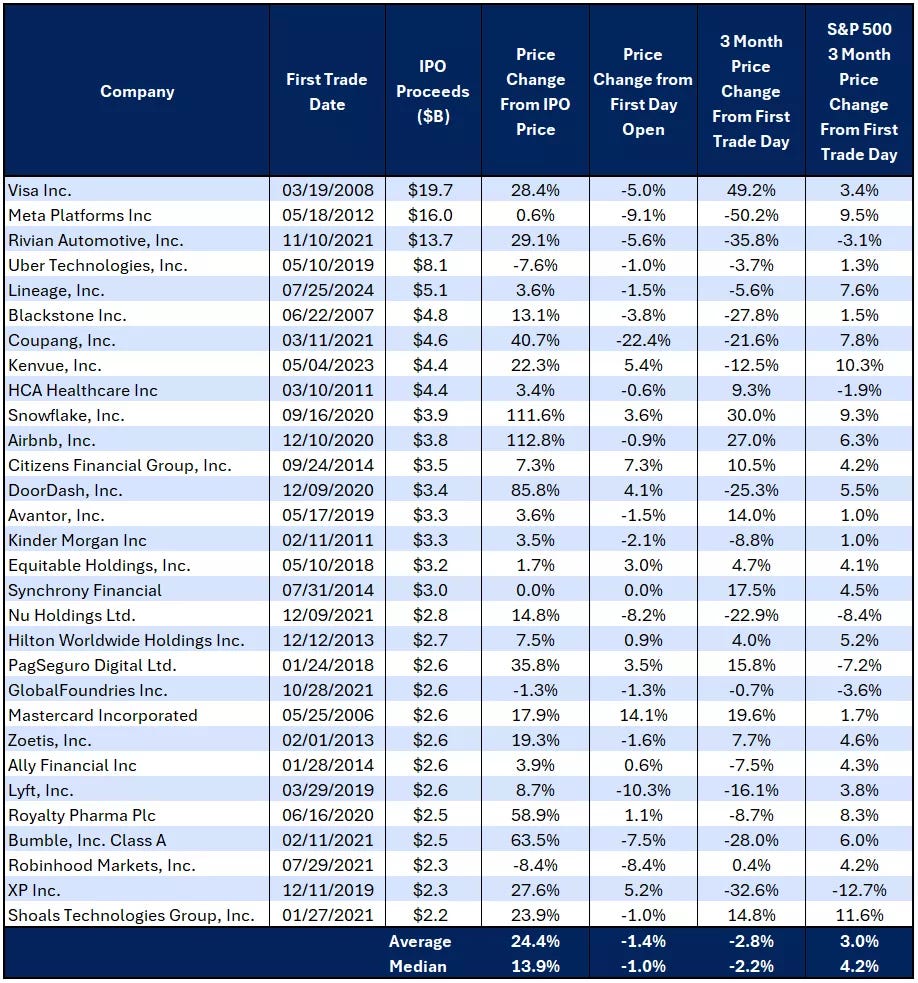

IPO performance

The data tells a consistent story.

On average, these stocks experienced a 24% price increase on the first day of trading compared to the security underwriters pricing (the offer price), helping to support the excitement associated with high-profile IPOs. However, the stock price declined by an average of 1.4% on the first day when compared to the day's opening price as shown. This is more aligned with what individual investors could experience trying to buy shares on the first day.

Source: Edward Jones

Read that again. The insiders got in at the offer price and saw a 24 percent pop. By the time you could buy, you were already down.

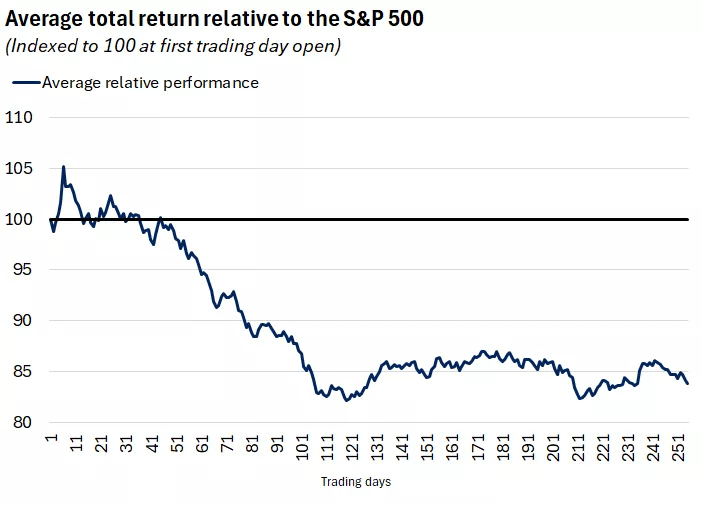

It gets worse from there.

These stocks, on average, underperformed the S&P 500 over the subsequent three-month period, as the IPO companies declined 2.8% on average while the S&P 500 increased 3%. This underperformance persisted over the first year of trading, suggesting that the short-term IPO enthusiasm does not necessarily translate into longer-term outperformance.

Source: Edward Jones

The buzz fades

The same pattern we have written in previous issues applies here. Smart money got in early. They will be selling into your excitement.

The best investors are not the ones chasing the loudest headlines. They are the ones who know when to wait.

So ask yourself this: are you investing in these companies, or are you funding the exit of the people who already did?

If you like my work, I invite you to share it with others.

Eric Chang

Calgary, Alberta

June 2, 2026

Copyright © 2026 EC Research Group.

No part of this publication may be reproduced, distributed, or transmitted in any form or by any means, including photocopying, recording, or other electronic or mechanical methods, without the prior written permission of the publisher, except in the case of brief quotations embodied in critical reviews and certain other noncommercial uses permitted by copyright law.

The information provided herein is believed to be accurate and reliable, but EC Research Group does not guarantee its accuracy or completeness. The content is for informational purposes only and is not intended to be a substitute for professional financial advice. EC Research Group is not a financial advisor and does not provide personalized financial advice. The views and opinions expressed in this publication are those of the author and do not necessarily reflect the official policy or position of EC Research Group. The content may be subject to change without notice and may become outdated over time. EC Research Group is under no obligation to update or revise any information presented herein.

Investments involve risks, and individuals should consult with a qualified financial advisor before making any investment decisions. Prospective investors should carefully consider the investment objectives, risks, charges, and expenses of any investment before investing.