Willing to miss out

When will I change my mind?

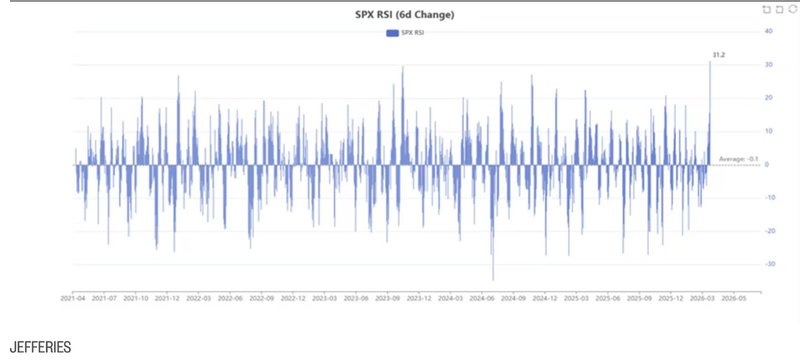

The stock market is now close to recovering to its previous all-time high.

For the past few weeks, I’ve been writing about the disconnect between reality and the stock market.

If anyone is keeping score, I’m getting a goose egg for anticipating a bigger market correction (15-20%) than what we’ve experienced since the start of the Iran-US-Israel war.

I’m not quite ready to throw in the towel yet.

Asymmetrical reward to risk

If you’ve been reading my newsletter for a while, you may know about my career in real estate.

When I meet new people, it’s easier to introduce myself as a real estate investor or developer.

After all, that’s what I’ve done over the past few years: develop infill multifamily buildings, acquire older real estate assets, and implement value-add strategies: Fix management. Bring rent on par with market. Renovate units to modernize them.

While those are visible from the outside, few people see the risk management work happening behind the scenes, as we dynamically adjust our strategies and approaches based on market conditions.

We aim to structure our real estate projects with an asymmetrical reward to risk profile.

What does asymmetrical reward to risk mean?

It means we’re looking for a combination of real estate asset, strategy, and market that gives us a higher potential return for the same amount of risk taken. Same construction build. Same price. But with a more favorable outcome over the holding period.

Here’s a real example.

We exited 3 projects over the past year. Two of those decisions came down to location.

We were monitoring new inventory being constructed in those neighborhoods. More supply creates future pressure on rent. More competition when those buildings complete.

We exited one project and rolled the capital into a different project in a superior neighborhood.

The cost of the build? The same.

But the premium neighborhood comes with higher lot prices, which naturally limits the number of new projects coming online over the next few years.

Because we rolled equity gains from the first project into the second, the higher lot premium didn’t change our total capital contribution.

With that maneuvering, we effectively lowered our risk while maintaining the same reward.

The reward: A multi-family asset that we anticipate to perform well over the 10 year hold period.

The risks: Anticipating a lower vacancy as there will be less comparable rental units competing for the same renters.

Same reward. Significantly lower risk.

That’s what asymmetrical reward to risk looks like for our investors.

Asymmetrical risk to reward

If you’ve been reading our recent newsletters, you know I’ve been extra cautious.

As a risk manager, my job is to identify potential risks and spot mispriced opportunities.

For every unit of risk we take on, I ask: what’s the associated payout?

When the downside risk to upside reward is highly unfavorable, we get conservative.

That’s exactly where I’ve been the past few weeks.

The downside risks have drastically increased since the war started. The upside reward remains relatively limited.

The upside for the global economy and stock market hasn’t changed.

The downside? There’s plenty.

Many traders are betting the war will be over soon. They’re buying up stocks. The result is a short-term short-covering rally, with hedge funds rushing in and the S&P 500 rocketing back close to its previous high.

Could this be an all-clear signal?

Possibly.

But I’d much rather wait for a bit more clarity before taking on more risk.

I’m not alone in this thinking. Famed hedge fund manager David Einhorn, who manages approximately $2.85 billion US in assets, recently wrote the following in his latest investor letter:

“It probably won’t surprise anyone that we are again putting capital preservation at the top of our priorities. With so little downside priced in, we are willing to risk missing out on a possible recovery to position ourselves to play more offense, should one of the downside scenarios materialize.”

That phrase: willing to risk missing out.

That’s where I am right now.

Will I change my mind?

Absolutely.

When there’s more certainty on the war. Whether there’s a resolution or a clear path to ensuring oil supply won’t be disrupted.

If the market breaks out of its previous high and holds, my conservative thesis is no longer valid. I’ll adjust back to looking for the market to move higher instead of playing defense.

But for now, the short squeeze dynamic is worth understanding clearly. Here are two articles worth reading:

A short-covering rally has stocks on shaky footing. Here’s what could happen next:

Short Sellers Squeezed Hard as Avis Shares Rocket 150%:

https://finance.yahoo.com/markets/stocks/articles/short-sellers-squeezed-hard-avis-191835924.html

The second article is particularly interesting.

In an economy that’s slowing down with skyrocketing oil prices, does anyone genuinely believe more people will be booking rental cars?

I don’t think so.

Yet the stock has gone up more than 300% in the past month.

The risk manager in me is screaming:

Wowzers! Watch out!

I’m willing to miss a little upside to avoid getting caught in the downside.

If you like my work, I invite you to share it with others.

Eric Chang

Calgary, Alberta, Canada

April 14, 2026

Copyright © 2026 EC Research Group.

No part of this publication may be reproduced, distributed, or transmitted in any form or by any means, including photocopying, recording, or other electronic or mechanical methods, without the prior written permission of the publisher, except in the case of brief quotations embodied in critical reviews and certain other noncommercial uses permitted by copyright law.

The information provided herein is believed to be accurate and reliable, but EC Research Group does not guarantee its accuracy or completeness. The content is for informational purposes only and is not intended to be a substitute for professional financial advice. EC Research Group is not a financial advisor and does not provide personalized financial advice. The views and opinions expressed in this publication are those of the author and do not necessarily reflect the official policy or position of EC Research Group. The content may be subject to change without notice and may become outdated over time. EC Research Group is under no obligation to update or revise any information presented herein.

Investments involve risks, and individuals should consult with a qualified financial advisor before making any investment decisions. Prospective investors should carefully consider the investment objectives, risks, charges, and expenses of any investment before investing.