Higher interest rates for longer

Three forces pushing rates higher

As a real estate investor for many years, I've learned to watch interest rates closely.

Rates set the cost of everything we do. They decide whether a project pencils out, whether a building cash flows, and whether an owner should sell. When rates move, the whole game changes.

We’ve been writing about the higher interest rate environment for a while now. You can catch up here:

If you've followed along, you already know where I stand. The era of cheap money is over.

Today I want to walk through why rates are climbing, and why I think they may stay higher for longer than most people expect.

How 3 different interest rate durations affect real estate

Here’s something people may not realize. The “interest rate” is not one number. The yield curve is really three different stories, and each one touches real estate in a different way.

The short term rate, or the front end of the curve, drives construction. Construction financing is usually tied to short-term interest rates and moves closely with central bank policy. When the central bank moves, construction loan moves with it.

The middle of the curve, what traders call the belly, reflects rates around the 5 year term. That is a common length for commercial mortgages and for Canadian residential mortgages. This affects the cost of holding real estate asset. The lower the rate, the more cash flow a property generates. The higher the rate, the tighter the squeeze on the same building.

The long end of the curve is usually tied to government debt between 10-30 years in duration. In the US, residential borrowers can choose a 15 year or a 30 year mortgage. The 30 year option is what created the “lock-in” effect the past few years. Millions of US homeowners took out mortgages at extremely low rates during the pandemic. Now they are stuck. Sell the house, and they trade a 3 percent mortgage for something far higher. So they don’t sell. Inventory dries up, and the whole market gums up.

Three Forces Pushing Rates Higher: Front-end

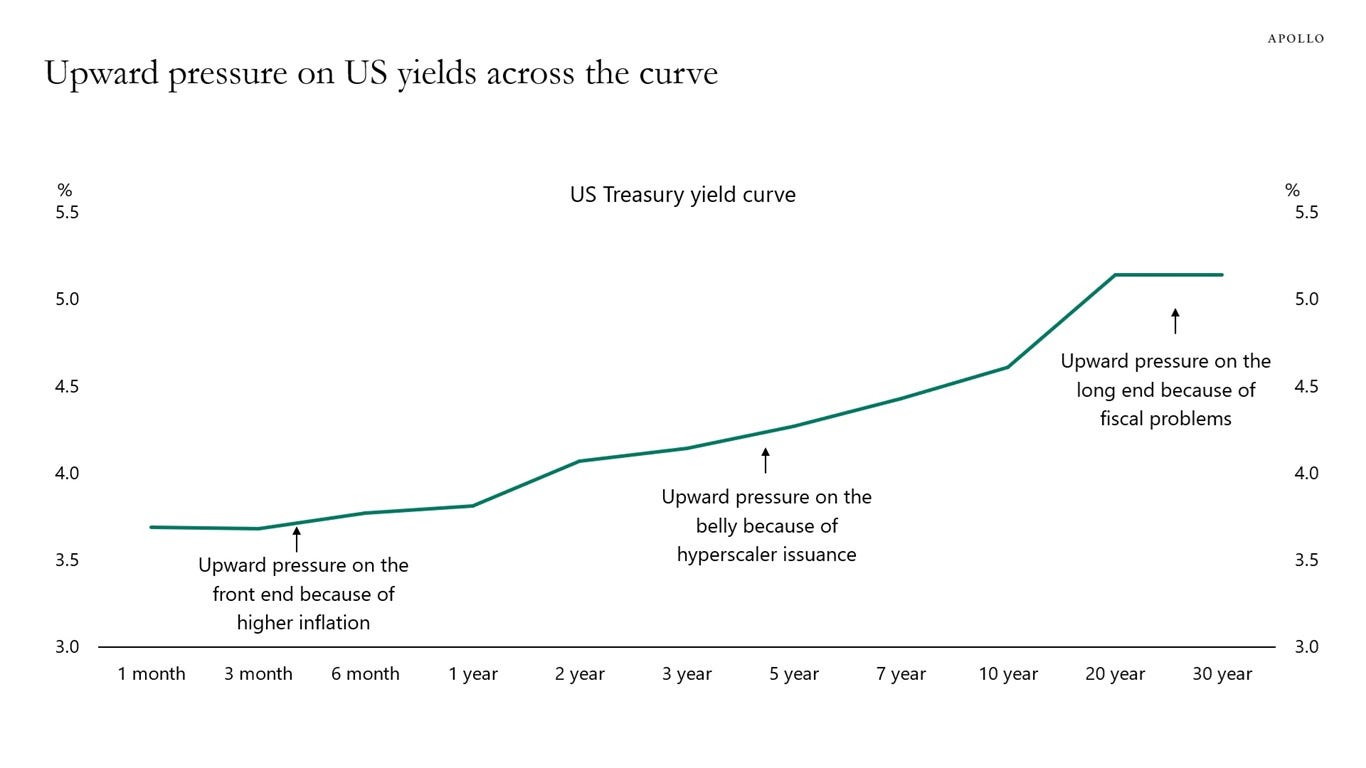

Apollo, a global asset management firm with roughly $1 trillion US under management, shared a chart on what is pushing interest rates higher in today’s environment.

Source: Apollo

The key insight is this. Rates are rising at every maturity, but for three different reasons. Understanding which force operates where matters, because it tells you the pressure is structural.

Start at the front end. Short dated yields anchor to the central bank rate and to the market’s expectation of where that rate eventually settles. Both have drifted up. Inflation is proving stickier while the US economy holds up well.

Now, some of the biggest banks are no longer talking about cuts at all. Bank of America and Deutsche Bank are now forecasting the Fed to raise rates in September, with Bank of America expecting three rate hikes totaling 75 bps in 2026: https://www.reuters.com/business/bofa-forecasts-75-bps-rate-hikes-2026-labour-market-resilience-new-fed-chair-2026-06-22/

No more cuts. Hikes may be coming ahead.

AI buildout creating pressure on higher rates

The belly of the curve is influenced by expectations for growth and inflation, but heavy corporate bond issuance can add upward pressure to yields and credit spreads. And lately, the hyperscalers (AI companies) have arrived as a force of their own.

The capital intensity of the AI buildout has turned the largest technology companies’ balance sheets into prolific bond issuers. They are terming out data center and compute spending in the intermediate maturities where the belly lives.

When the highest quality names flood that part of the curve with record amount of debts, yields rise for the market to absorb the supply. There’s too much debt hitting the market at the same time.

The AI story everyone is celebrating in the stock market may be pushing up the cost of borrowing for everyone else, including real estate developers who has nothing to do with AI.

Now the long end

The US Treasury continues to issue heavily to fund persistent deficits. The supply of new government debt keeps coming, and it is not slowing down.

On the other side, the Fed has stepped back as a buyer.

So long rates rise to compensate investors for holding debt the central bank no longer wants. Less demand, more supply, higher yields. The big money printer is no longer running at full speed.

The bottom line is that while these forces overlap, but each is currently exerting the greatest pressure on a different part of the curve, pushing rates higher: sticky inflation at the front, hyperscaler issuance in the belly, and a supply and demand imbalance at the long end. Different causes, same outcome: higher rates.

For real estate operators and developers, this is a more challenging environment to navigate. Construction costs more to finance. Holding costs more to carry.

The higher rate environment may stay around longer than the optimists hope.

Not to mention, the fallout from the war in the Middle East is only starting to show up. Those price increases are still trickling through the supply chain.

Time to be extra careful as real estate investors today.

If you like my work, I invite you to share it with others.

Eric Chang

Calgary, Alberta

June 23, 2026

Copyright © 2026 EC Research Group.

No part of this publication may be reproduced, distributed, or transmitted in any form or by any means, including photocopying, recording, or other electronic or mechanical methods, without the prior written permission of the publisher, except in the case of brief quotations embodied in critical reviews and certain other noncommercial uses permitted by copyright law.

The information provided herein is believed to be accurate and reliable, but EC Research Group does not guarantee its accuracy or completeness. The content is for informational purposes only and is not intended to be a substitute for professional financial advice. EC Research Group is not a financial advisor and does not provide personalized financial advice. The views and opinions expressed in this publication are those of the author and do not necessarily reflect the official policy or position of EC Research Group. The content may be subject to change without notice and may become outdated over time. EC Research Group is under no obligation to update or revise any information presented herein.

Investments involve risks, and individuals should consult with a qualified financial advisor before making any investment decisions. Prospective investors should carefully consider the investment objectives, risks, charges, and expenses of any investment before investing.