Socialistic Capitalism

Welcome to the new financial market

We’re progressing into what I believe is the next version of Capitalism: Capitalism 2.0.

Last week we wrote about Canada’s launching a Sovereign Wealth Fund.

This week, we’re going to compare Canada to other parts of the world. Because a quiet but significant trend is emerging across developed countries. One that I believe represents the next version of Capitalism. Call it Capitalism 2.0. Or Socialistic Capitalism.

Whatever you call it, the implications for investors are enormous.

Government's increasing involvement in the financial markets

As many of my long-term subscribers know, I have been in real estate for many years, running a moderate-sized real estate portfolio and real estate development business in the multifamily asset class based in Alberta, Canada.

Over the past few years, the role the Government of Canada plays in the Canadian housing market has expanded significantly.

Policies and initiatives through Canada Mortgage and Housing Corporation (CMHC) have been enacted to incentivize development of Purpose Built Rentals. Through high leverage (up to 95% Loan to Value), extended amortization (up to 50 years), and the Government’s increasing purchases of Canada Mortgage Bonds, representing close to 50% of new issuances in 2025, the government has effectively positioned itself as a price-setter (interest rate) in the mortgage market.

The Government of Canada announced on November 21, 2023 that it will begin purchasing up to C$30 billion of Canada Mortgage Bonds annually, commencing in 2024. In the 2024 calendar year, the Government of Canada purchased a total $29 billion of the $58 billion of fixed-rate Canada Mortgage Bonds primary issuances. The Government of Canada has indicated that it will continue to participate in all offerings of fixed-rate 5-year and 10-year Canada Mortgage Bonds proposed for 2025 and that it will target the purchase of 50% of such fixed-rate Canada Mortgage Bonds issued in 2025, although the amount it purchases of a particular new issuance may be more or less than 50% of that issuance

The launch of Canada’s Sovereign Wealth Fund is another step in this same direction. While I welcome the strategic intent of using capital to create tactical advantage for Canada, it represents yet another expansion of government into territory that was previously market-driven.

To be fair, Canada is not alone in this.

A refresher on Socialism

James K. Glassman, a senior fellow at the American Enterprise Institute, wrote an article as far back as 1999 raising the alarm about what happens when governments begin taking ownership stakes in private companies. This was before the Obama-era bailouts of Detroit automakers. Before recent developments where the US government took equity positions in select private companies, including Intel.

His warning is worth reading carefully:

Ownership of stock by the government raises deep and troubling issues.

[...]

I do not want to sound overly dramatic, but, by definition, the plan is a step toward the dictionary definition of socialism: government ownership of the means of production.

Thus, Congress must first answer this question: Should the federal government have an ownership stake in private corporations?

Source: https://www.aei.org/research-products/testimony/government-investing-in-the-stock-market/

That question was intended to be a debate in 1999.

Today, it’s now widely accepted and even celebrated by the President.

A President who represents a Party that has championed free market in recent memory.

The Center for Strategic and International Studies has also reported on the significant shift in U.S. industrial policy, noting the expanding footprint of federal equity investments in strategic companies. You can read their full analysis here: Understanding Federal Equity Investments in Strategic Companies.

The US government now holds direct equity stakes in private companies it deems strategically important. That is a meaningful shift from the past.

Japan has gone to the extreme in practicing Socialistic Capitalism

Before you brush off what’s happening in Canada and the US as minor, let me show you the extreme end of the spectrum. I’ll use a country I’m currently visiting as the example.

Since 2010, the Bank of Japan (BOJ) began purchasing Japanese Exchange-Traded Funds (ETFs), these are investment products similar to mutual funds that invested in domestic Japanese companies.

The BOJ has a reported book value of 37 trillion yen (around $243 billion) in ETF holdings on its balance sheet, with an estimated market value of 70 trillion yen to 80 trillion yen. This amounts to roughly 7% of Japan’s stock market capitalization.

Source: https://cetex.org/news/the-boj-must-define-a-strategy-for-its-etf-holdings-not-just-its-sales/

Bank of Japan currently owns roughly 7% of the entire Japanese stock market.

That also represents roughly 80% of Japan’s entire exchange-traded funds.

Read that again:

The Bank of Japan owns roughly 80% of the Japanese ETF market!

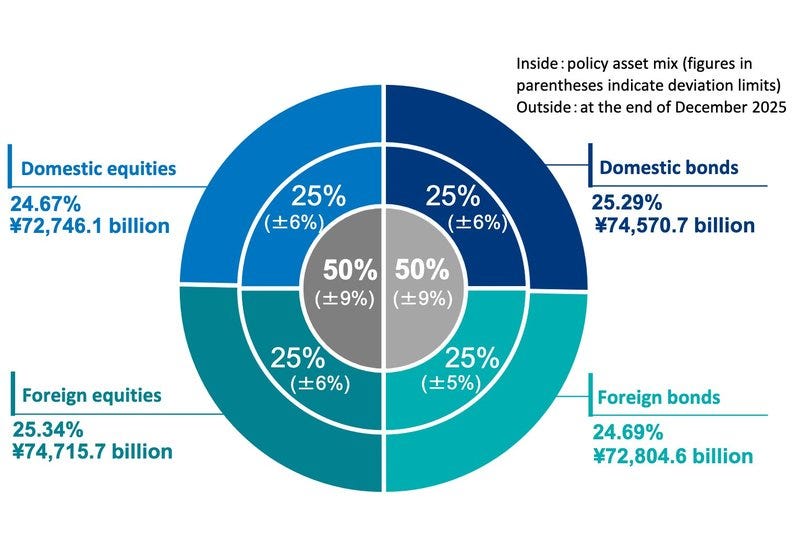

And that’s before factoring in the Japanese Government Pension Investment Fund (GPIF), which holds roughly 73 trillion yen in Japanese companies. That’s another 6% of the entire Japanese stock market.

Image Credit: GPIF

Combined, the Japanese government controls roughly 13% of its entire domestic stock market. A market that, without this intervention, could function very different.

What's the problem?

History has shown us what happens when socialism takes hold: highly inefficient capital allocation, followed by economic decline.

Now, Capitalism 2.0 isn’t pure socialism. But it introduces the same core problem. When government steps in as a perpetual asset buyer, asset prices detach from their fundamentals. The price discovery mechanism breaks down.

Price discovery is the continuous, market-driven process of determining the fair value of an asset through the interaction of buyers and sellers.

When one buyer has essentially unlimited resources, and that buyer is the government, the market stops functioning as a truth-telling mechanism.

Asset prices stay inflated. Not because of genuine demand. Because of policy.

Make no mistake: this is not healthy in the long run.

It took the Japanese government owning roughly 13% of its entire stock market to keep a fragile market from collapse. That’s a market that was previously on life support, brought back to life through intervention.

The longer investors grow comfortable with the idea that government will always bail them out, the more it encourages reckless speculation. Risk is mispriced. Bad decisions get rewarded. And the eventual correction, when it comes, is far more painful than it would have been without all the artificial support.

That’s a topic we’ll unpack in future issues.

For now, the question worth sitting with is this: If price discovery is compromised, how do you know what anything is actually worth?

If you like my work, I invite you to share it with others.

Eric Chang

Tokyo, Japan

May 5, 2026

Copyright © 2026 EC Research Group.

No part of this publication may be reproduced, distributed, or transmitted in any form or by any means, including photocopying, recording, or other electronic or mechanical methods, without the prior written permission of the publisher, except in the case of brief quotations embodied in critical reviews and certain other noncommercial uses permitted by copyright law.

The information provided herein is believed to be accurate and reliable, but EC Research Group does not guarantee its accuracy or completeness. The content is for informational purposes only and is not intended to be a substitute for professional financial advice. EC Research Group is not a financial advisor and does not provide personalized financial advice. The views and opinions expressed in this publication are those of the author and do not necessarily reflect the official policy or position of EC Research Group. The content may be subject to change without notice and may become outdated over time. EC Research Group is under no obligation to update or revise any information presented herein.

Investments involve risks, and individuals should consult with a qualified financial advisor before making any investment decisions. Prospective investors should carefully consider the investment objectives, risks, charges, and expenses of any investment before investing.